This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

CMU Trends Digital

Trends: Plenty of digital debates

By Chris Cooke | Published on Wednesday 15 January 2014

It feels like there weren’t any major developments in digital music in 2013, with most column inches dedicated to the ongoing debate over the royalties paid by the streaming music platforms (focused on Pandora in America and Spotify in Europe). Though a more interesting discussion was also being had away from the spotlight about what kinds of digital services can and will succeed.

THE DOWNLOAD MARKET: OWNERSHIP OF MUSIC

Although many noted that growth in the ‘a la carte download market’ – a sector still led by the iTunes Store of course – had slowed considerably of late, and indeed seems to have peaked in the US, it’s worth noting that overall this digital revenue stream – the ‘ownership model’ – is still by far the biggest. And as the new HMV re-entered the digital market in October, it did so with a conventional iTunes-style download store, insisting that for the mainstream consumers it targeted this remained the most attractive proposition.

It’s easier running a download store in some ways, because the business model has been pretty much standardised. You sell tracks on a pay-per-download basis with 99p per track the average price point, downloads will be DRM-free MP3s (or AACs in iTunes’ case) encoded at 256 or 320kbps, and tracks, once bought, will be accessible via a digital locker on multiple devices. Some clever pricing can then be used to incentivise consumers to buy albums instead of singles, including compilations, which have seen something of a resurgence this year. The downside, of course, is that iTunes dominates, and it’s hard to distinguish yourself from the market leader.

THE STREAMING MARKET: ACCESS TO MUSIC

But the really impressive growth stats of late, of course, have come from the streaming platforms, which offer ad-funded or subscription-based ‘access’ services. Some reckon that, ultimately, these ‘access platforms’ will come to dominate in digital music, with ownership-based download stores going into decline.

And in some markets (mainly Scandinavian) and for some labels (mainly indies), streaming revenue is already topping download income. Though overall, worldwide, the latter is still much more substantial, and the streaming revenue that is coming in is currently subsidised, to an extent, by the venture capitalists and tech/mobile companies who are backing the loss-making streaming firms.

Nevertheless, streaming revenue will continue to grow for the foreseeable, and those revenues may well be maintained as the market comes of age. Though some reckon access and ownership services will still happily co-exist, the former satisfying serious music fans, the latter more casual consumers. Though a pessimist might point out that most streaming business models also rely on eventually engaging that more casual consumer.

But, even if the streaming market is as yet far from stable, it now plays a significant role in the music rights sector, and that role will only increase in significance in the coming years. Though, of course, whereas most download stores operate in pretty much the same way, in the streaming space there is lots of variation between services (and, indeed, most services are constantly refining their business models).

The two key variations in streaming are…

Listen v Access

Pandora-style ‘personalised radio’ services versus Spotify-style ‘fully on-demand’ set-ups, a distinction that analyst Mark Mulligan refers to as ‘listen v access’. Listen services currently dominate in the US, while access services generally lead in Europe.

For serious music fans the fully on-demand model is almost certainly more attractive, though some argue that more casual consumers find the size of Spotify-style catalogues and the requirement to pick from them off-putting, and therefore maybe more attracted to the simpler if less sophisticated listen services, which are also cheaper to run because labels charge higher royalties to more interactive platforms.

The differences between the US and European streaming markets are interesting, though the dominance of ‘listen’ platforms in the former is almost certainly because of American copyright law, which forces the labels to license such services (but not ‘access’ platforms) through the SoundExchange collective licensing system, and therefore gave Pandora et al a considerable head start while the record companies dithered over other streaming systems.

Though the dominance of one model or the other may also be partly down to which brands happen, for whatever reason, to gain traction. It will be interesting to see what impact the Beats-branded streaming platform, a fully on-demand service, will have in the US, and likewise how iTunes Radio, a listen service, will fair when it is rolled out beyond the American market.

Ad Funded v Subscription

The biggest music streaming service in the world is YouTube, even if a significant chunk of the content being streamed on the Google-owned platform is actually controlled by the Universal/Sony joint venture Vevo. Both YouTube and Vevo are, of course, ad-funded free-to-access services, which is, in a big part, the reason for their success.

The per-play royalties they pay out are tiny, though both have generally avoided being mentioned in the aforementioned streaming royalties debate; partly because many in the music industry still see anything involving video as primarily a promotional opportunity with licensing income a happy aside, and partly because overall YouTube and Vevo are paying in significant sums into the music-rights sector.

Away from the video platforms, freemium audio streaming – although perhaps originally seen as a viable business in itself – has generally been used of late as a way of promoting premium subscription options, certainly in the fully on-demand space (it’s possible ad-funded can work alone for ‘listen’ services).

Many of Spotify’s competitors have borrowed its marketing approach of offering freemium streaming with ads in the hope that users will love the experience, and gladly hand over five or ten pounds a month to lose the irritating commercials.

Though if freemium is just marketing for Spotify et al, and they really need to sell subscriptions to work commercially, that makes the always free YouTube/Vevo a problem competitor, especially if Google upgrades the YouTube smartphone app in 2014 so that it matches the extra mobile functionality offered to premium users by the audio streamers. And, it seems, the youth market where YouTube is particularly strong doesn’t care about the ads, which have become more abundant and longer in the last year on the video sites (unless, that is, the kids are employing ad-blocking plug-ins on their browsers, which would make YouTube on a mobile less attractive, where ads cannot be so easily edited out).

Moving forward ad-funded and subscription services will almost certainly co-exist, the challenge for the digital music companies though is working out what role freemium plays in their businesses.

THE ROYALTIES DEBATE

And then there is the aforementioned digital royalties debate. In the US, Pandora’s ongoing efforts to reduce the royalties it pays to the record companies and music publishers was criticised by pretty much everyone in the music industry in 2013. Pandora maintains that its royalty burden is unfair when compared to FM radio (which pays only the publishers in the US) and satellite radio (which pays the labels too, but on more favourable terms than online services).

And Pandora reckons that radio is its main competitor, which – as streaming reaches the car dashboard – it increasingly is. But the industry insists that Pandora’s founders have built a multi-billion dollar business, and cashed-in bigtime when the firm floated in 2011, on the back of the music industry’s content and if anything should be paying higher royalties than they currently do.

In Europe, where Pandora doesn’t operate, the royalties debate centred on Spotify. Well, on all streaming services really, but as the most high profile (in the UK at least), Spotify got the brunt of the anger. Radiohead’s Thom Yorke and his producer collaborator Nigel Godrich became the poster-boys of the anti-Spotify brigade, while a string of other artists entered the debate, some supporting the streaming platform, others sharing the Godrich Yorke Concern.

Unlike with the Pandora debate in the US, the record labels and music publishers are, with a few exceptions (Ministry Of Sound most notably), pro the Spotify business model. Of course many labels have shares in Spotify and stand to win when it floats or is sold. But even most key players in the management community – including Radiohead manager Brian Message – insist that the streaming services have an important role to play in the growth of digital music.

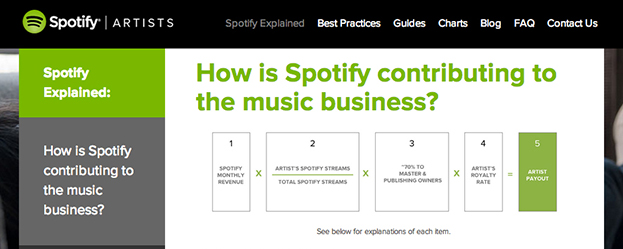

After months of being dissed by high profile artists, Spotify responded in December by launching a new website aimed at the artist community, offering more transparency on how the streaming service pays its royalties and access to valuable data about how any one act is performing on the platform.

Commitments were also made to enhance sell-through on Spotify, so that artists can generate extra revenue through tickets and merch, a flippin obvious add-on that no one in the streaming space has properly embraced as yet, possibly because of the challenge of doing the necessary deals in such a fragmented music industry.

The UK’s Music Managers Forum and Featured Artists Coalition, who together represent many of Spotify’s critics, welcomed the new website and other commitments made by the streaming service. Though you feel four issues remain as we enter 2014…

The overstatement of streaming as the saviour of the music business

Spotify is, in many ways, a victim of its own success, in that it has to hype itself as the “future of music” to maximise value when the inevitable IPO or mega-sale occurs, but in doing so artists often over-estimate the importance of the service in their own businesses, and then panic when they see the royalties they receive.

The challenge when the streaming start-ups pass first sale

If Spotify thinks that this year has had its PR stresses, the real challenge for all the streaming music start-ups will come after their IPOs or big acquisitions, when profitability rather than valuation becomes key. And as with Pandora in the US, if any of these services go public, they’ll almost certainly find themselves having to negotiate royalty rates down (to satisfy shareholders) while artists and rights owners, aware of market cap valuations and senior executive pay packages, might start calling for higher payments.

Artists split on digital

Meanwhile, the streaming royalties debate has another dimension, being fought out by heritage artists in the American courtrooms: how much of the money Spotify pays the labels should be passed onto the artists. For veteran acts with pre-web record contracts that don’t mention digital income, this debate has gone legal many times already Stateside, and similar litigation could soon occur in Europe. Newer artists whose streaming royalties will be set out in contract can’t exploit any legal ambiguities, but some managers are arguing that the real problem with Spotify royalties is that some labels (especially the majors) hold on to too much of the money.

Recording v publishing split

And then there is the labels v publishers angle. Nigel Godrich, as a producer, likely won’t be placated by Spotify’s sell-through add-ons for artists; because non-performing producers and songwriters don’t have other products to sell, and rely much more on good old fashioned copyright income. But songwriters and publishers, in the main, are currently receiving a much smaller cut of the digital pie. As featured artists start to generate ever higher income from merch, brand partnerships and D2F services, and as labels are increasingly cut into those revenue streams, expect the songwriting and publishing community to start demanding an overhaul of how digital money is split between the rights owners.